In particular we focus on getting the loan structure right the first time, choosing which lenders to use in the right order (yes this is important) and finally getting our clients the best deal possible.

Case Study: Common Debts with Family Members

Marty McDonald

The problem:

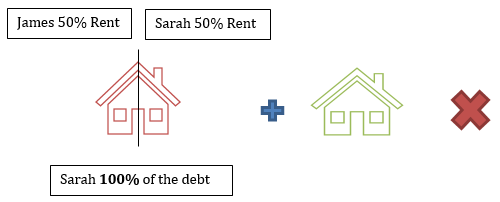

Recently we had a client Sarah come to us looking to buy her own home. She already owned an investment property 50/50 with her brother James. Sarah did not qualify for a new loan with her current lender because that lenders policy is to take 100% of her joint loan commitment into account while only allowing 50% of the rental income received on that property to be included in their assessment. This was even after proving to the lender that her brother paid 50% of the loan repayments and other costs.

The solution:

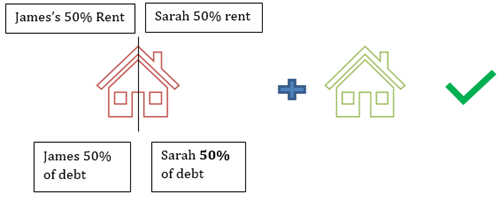

We found a lender for Sarah that had a Common Debt Reducer Policy. This meant that if we could show that her brother was self-supporting and that he could manage paying his half of the investment loan repayments then they would take just 50% of the existing loan into account for Sarah. She would need to show she could service the new loan in her own right and half of the existing loan.

We found a lender for Sarah that had a Common Debt Reducer Policy. This meant that if we could show that her brother was self-supporting and that he could manage paying his half of the investment loan repayments then they would take just 50% of the existing loan into account for Sarah. She would need to show she could service the new loan in her own right and half of the existing loan.

This is an example of the niche lending policies where Mortgage Experts knowledge can help clients achieve their property goals.

About the Author: Marty McDonald is principal of mortgage broker “Mortgage

Experts”. Marty specialises in assisting active property investors with loan structuring advice and

implementation as well as helping credit worthy borrowers with slightly outside the box income and employment

situations. Find Marty on

Facebook and

LinkedIn.

< back

Recent Posts

- The “Housing Crisis” and Capital Gains Tax (CGT) changes? Thoughts…

- Is now the time to access equity? APRA changes coming + Interest rate outlook

- Government Guarantee Scheme – an update on the changes from 1st October 2025

- Limited Deposit and don’t qualify for the government guarantee scheme? Up to 100% LVR loans available

- Government grants and schemes - to help you into the market

- Is Darwin property about to go Boom?

- Comparing interest rates (Western Democracies)

- Stage 3 Tax cuts - how will it effect your borrowing capacity?

- Property Share Loan Structure

- SMSF Property Investing & Lending - Back on the agenda